| |

|

|

|

|

|

|

|

|

|

![]()

●

契約者データ管理(Subscriber Data Management)でより迅速なサービスの提供を目指す

オペレータ

2010年8月10日、カリフォルニア、キャンプベル- Infonetics Researchは今月、アナリストによる次世代OSS・ポリシー市場に関する継続的調査サービス(Continuous Research Service:CRS)の一部として、SDM導入戦略 : グローバルサービスプロバイダ調査を発表した。

本調査は、投資の主な要因、ベンダーの選別基準、Subscriber Data Management (SDM)の統合作業などを含む、オペレータによる契約者データ管理の展開戦略について情報提供するものである。

アナリスト分析

「契約者情報を一元化する作業はオペレータにとって重要な目標であるため、ますます多くのオペレータが契約者データ管理(SDM)を利用し始めている。最近の調査結果によれば、オペレータは、新サービスの迅速な導入やクロスセリング・アップセリングの機会をより多く発見する上で、SDMが有用なツールであると見ている。一元化して分析した契約者情報があれば、顧客セグメンテーション、マーケティング、顧客維持、ロイヤリティ・プログラムなどを含めたサービス展開戦略において、オペレータはより洗練されたアプローチを取ることが可能となる。」

分析: Infonetics Research次世代OSS及びポリシー担当ディレクティング・アナリスト、Shira Levine

調査概要 : SDM導入戦略

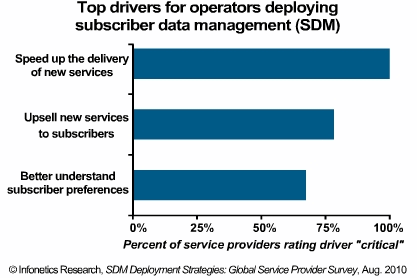

- オペレータが契約者データ管理ツールを導入するのは、新サービスの提供速度を上げたり、契約者に対して更に高価格な新サービスを販売したり、契約者の選好をより深く理解することなどが主な動機である。

- SDMの導入が成功するかどうかは、経営者レベルの支援とデータ設備の連携などに掛かっている。

- マシン・トゥ・マシン(M2M)サービスは、SDMで最も成長著しい分野であり、調査回答者の75%が2013年までにSDMを利用してM2Mを支援する計画を持っている。

- オペレータは、特にID管理サーバやホーム加入者サーバなどの補完システムと共同でSDMを展開している。

調査について

SDM戦略調査において、Infonetics Researchは、契約者データ管理システムを現在有するか、または2011年までに導入する計画を持つ北アメリカ、EMEA、アジア太平洋のテレコムサービスプロバイダに対し、その購買担当者にインタビュー調査を実施した。回答者は、HLR、HSS、ngHLRを含め、自社のSDMソフトウェアや統合サービス、契約者データベースについて詳細な知識を持つ者が対象となった。調査に参加したサービスプロバイダは、通信業界から幅広く選び出され、北アメリカで最大規模を誇るオペレータが2社、アジア最大のオペレータが1社、それらより規模は劣るが急成長しつつあるヨーロッパと北アメリカのワイヤレス・オペレータ、そしてマシン・トゥ・マシン(M2M)サービスを提供する複数のオペレータが調査対象となった。

サービスデリバリープラットフォームが主流に

サービス提供基盤は当初、コンテンツサービスの提供を可能とする基盤として目されていたが、SDP市場が成長し続けるに連れ、柔軟なサービスの提供を可能とする、支払いの一括請求やシングル・サインオンなどを含め、オペレータがSDPで支援するアプリケーションや機能において、一層洗練されたアプローチが取られるようになっている。こうしたアプローチは、SDPの主流となるだろう。

一括請求(Convergent Charge)の市場は2014年に26億円規模となる可能性

経済は回復し、オペレータは再び投資を開始するかもしれないが、過去に見られたように請求システムの移行計画を全面的に実施する企業はほとんどないだろう。しかし、既存企業の請求システムは、前払い制も後払い制も含めますます時代遅れとなってきており、新しく統合されたビジネスモデルの支援に必要となる柔軟性やスピード、リアルタイムの処理能力などが不足してきている。一括請求システムを利用すれば、大規模な請求システムの変更に掛かるコストを負担せずに、そして更に重要なポイントとして、垂直統合されたシステムを新たに事業環境へ導入すること無く、オペレータは上記の問題に取り組むことが可能となる。オペレータは、真に統合化されたサービスを導入し、アップセリングやクロスセリングによってサービスの提供を促進し、顧客体験を向上することなどが、迅速かつ効果的な方法で全て同時に行えるようになる。

原文

Operators seek to launch services faster with Subscriber Data Management (SDM)

Campbell, CALIFORNIA, August 10, 2010-As part of its Continuous Research Service (CRS) series of analyst notes and surveys about the next gen OSS and policy market, Infonetics Research this month published SDM Deployment Strategies: Global Service Provider Survey. The survey provides insight into operators’ subscriber data management deployment strategies, including the primary drivers behind their investments, vendor selection criteria, and SDM integration efforts.

ANALYST NOTE

“Creating a consolidated source of subscriber information poses a significant challenge to operators, which a growing number of operators are overcoming with the help of subscriber data management (SDM). The results of our recent survey show that operators view SDM as a valuable tool for quickly rolling out new services and for better identifying cross-sell and upsell opportunities. With consolidated and analyzed subscriber data, operators can take a more sophisticated approach to their service delivery strategies, including customer segmentation, marketing, and customer retention and loyalty programs,” notes Shira Levine, directing analyst for next gen OSS and policy at Infonetics Research.

SURVEY HIGHLIGHTS: SDM DEPLOYMENT STRATEGIES

- The top drivers for operators to deploy subscriber data management tools are to speed up the delivery of new services, upsell new services to subscribers, and to better understand subscriber preferences

- The success of any SDM initiative depends on executive-level endorsement and collaboration across data silos

- Machine to machine (M2M) services represent a hot growth area in the SDM space, with 75% of respondents reporting plans to use SDM to support M2M by 2013

- Operators are deploying SDM hand-in-hand with complementary systems, particularly identity management and home subscriber servers (HSS)

ABOUT THE SURVEY

For the SDM strategies survey, Infonetics Research interviewed purchase decision-makers at telecom service providers in North America, EMEA, and Asia Pacific that have a subscriber data management solution currently deployed or plan to have one by 2011. Respondents also have detailed knowledge of their company’s SDM software and integration services and subscriber databases, including HLR, HSS, and ngHLR. Service providers participating in the study represent a broad cross-section of the communications industry, including two of the largest operators in North America and one of the largest operators in Asia, smaller emerging wireless operators in Europe and North America, and several operators with strong machine-to-machine (M2M) offerings.

| Service delivery platforms going mainstream |

While service delivery platforms were initially viewed as platforms to enable content services, as the SDP market continues to mature, we're seeing operators taking a more sophisticated approach to the applications and capabilities they're using SDPs to support, including convergent billing and single sign-on to enable flexible service bundles. This kind of approach will take SDPs mainstream.

| Convergent charging market a $2.6 billion opportunity in 2014 |

The economy may be improving and operators may be investing again, but very few will be doing the full-scale billing transformation projects that we saw in the past. Yet it has become clear that their existing billing systems-both prepaid and postpaid-are increasingly falling short, lacking the flexibility, speed and/or real-time capabilities required to support new convergent business models. Convergent charging allows operators to address that challenge without the high cost associated with a large-scale billing replacement and, even more important, without introducing additional vertically-integrated silos into their operational environments. They can quickly and efficiently roll out truly bundled services, up-sell and cross-promote services, and improve the customer experience at the same time.