| |

|

|

|

|

|

|

|

|

|

![]()

●

Session border controllerの調査によりVoIP相互接続でのSBCの使用増加が明らかに

2010年10月18日、カリフォルニア、キャンプベル―市場調査会社のInfonetics Researchは今日、SBC展開戦略 : 世界サービスプロバイダ調査の抜粋を公表した。本レポートは、サービスプロバイダのVoIP及びIMS 市場に関する一連の調査報告の一部であり、session border controllersを利用したアプリケーションやSBCの重要な機能、セキュリティの課題、市場ではどのベンダーが利用されているかなどについて、広範囲のサービスプロバイダから戦略的な概要を掴むものである。

アナリストノート

「今年のsession border controller調査において最も興味深かった4つの発見は、組込み用SBCに対する関心が増加していること、他のサービスプロバイダとの相互接続にSBCが増々利用されて来ていること、新しいSBCの展開においてフィックスド・モバイル・コンバージェンスとワイヤレスアクセスの堅調な増加が見込まれること、サービスプロバイダが依然としてセキュリティ侵害に高い関心を抱いていることである。SBCは、次世代音声ネットワークにおいて決定的な要素になっている。SBCは更なる機能性を獲得しながら、トラフィックマネージャーやポリシーエンジンへと進化している。」とInfonetics ResearchのVoIP及びIMS担当ディレクティングアナリストのDiane Myersは説明する。

SBC調査ハイライト

- 現在、サービスプロバイダに最も使用されているアプリケーションはSIPトランキングである。

- 2012年に最も使用されていると見込まれるSBCアプリケーションはサービスプロバイダ間の相互接続であり、この動きは世界中の音声ネットワークの全IP化が進んでいるために増加している。

- SBCで最も早く成長しているアプリケーションは、第4世代の音声、第3世代のモバイルVoIP、リッチ・コミュニケーション・スイート(RCS)を含めたフィックスド・モバイル・コンバージェンス(FMC)とワイヤレスアクセスである。

- 孤立個別SBCへの支出が大勢を占め続けるが、増々多くのサービスプロバイダがネットワークの構成要素に組込みSBCを使用することを考え始めている。

- 自由回答の質問では、95%のサービスプロバイダから「トップSBCベンダー」として名が挙がったのはSBC市場のシェアリーダーであるAcme Packet であった。

- 回答したサービスプロバイダの3分の1は、トップSBCベンダーとしてGENBANDの名も挙げた。

- 将来のSBC購入先としてどのベンダーを評価しているかという質問では、サービスプロバイダのほとんどはCisco、Alcatel-Lucent、Juniperなど組込みSBCの製品を多く持つ新興ベンダーの他にAcme Packetの名を挙げた。

調査について

SBC展開戦略の調査でInfoneticsは、世界のテレコムCAPEXの26%を占め、世界のテレコム収入の31%を占める43社のサービスプロバイダに対し、SBC購入の意思決定担当者にインタビューを実施した。サービスプロバイダは、様々な地域(44%がヨーロッパ/中東/アフリカ、33%が北アメリカ、16%が中央・ラテンアメリカ、7%がアジア太平洋)とキャリアタイプ(37%が競合オペレータ、35%がインカンバントキャリア、19%がケーブルオペレータ、9%がワイアレス)を代表している。

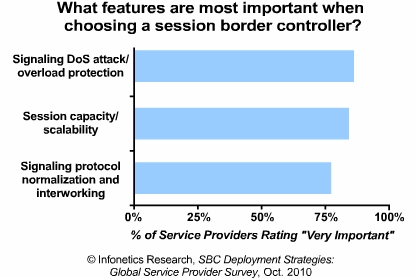

サービスプロバイダは、最も重要なSBC機能やSBCアプリケーションからセキュリティ問題、予定計画、ネットワーク・ロケーションの計画、SBCベンダーの印象など幅広い質問に回答した。

(原文)

Session border controller survey shows growing use of SBCs for VoIP interconnection

CAMPBELL, California, October 18, 2010-Market research firm Infonetics Research today released excerpts from its SBC Deployment Strategies: Global Service Provider Survey. The report, part of a series on the service provider VoIP and IMS market, captures a strategic overview from a wide range of service providers about applications using session border controllers, important SBC features, security issues, and which vendors are being utilized in the market.

ANALYST NOTE

“Four of the most interesting findings in this year’s session border controller survey are that there’s growing interest in embedded SBCs, that SBCs are increasingly used to interconnect to other service providers, that fixed-mobile convergence and wireless access are solid growth prospects for new SBC deployments, and that service providers remain highly concerned about security breaches. SBCs have become a critical element in next generation voice networks. They have evolved into traffic managers and policy engines, taking on more and more functionality,” notes Diane Myers, directing analyst for VoIP and IMS at Infonetics Research.

SBC SURVEY HIGHLIGHTS

- SIP trunking is the #1 SBC application currently used by service providers

- The #1 SBC application expected in 2012 is interconnection between service providers, a growing phenomenon as the world’s voice networks increasingly become all IP

- The fastest-growing applications for SBCs are fixed-mobile convergence (FMC) and wireless access, including 4G voice, mobile VoIP over 3G, and Rich Communication Suite (RCS)

- Standalone dedicated SBCs continue to dominate deployments, but an increasing number of service providers are looking at deploying embedded SBCs in a range of network elements

- In response to an open-ended question, SBC market share leader Acme Packet was named by 95% of service providers as a "top SBC vendor"/li>

- GENBAND was also named a top SBC vendor, by about a third of respondent service providers

- When asked which SBC vendors they are evaluating for future SBC purchases, service providers overwhelmingly named Acme Packet, as well as emerging vendors with more of an embedded SBC product set, such as Cisco, Alcatel-Lucent, and Juniper

ABOUT THE SURVEY

For the SBC Deployment Strategies Survey, Infonetics interviewed SBC purchase decision-makers at 43 service providers that represent 26% of worldwide telecom capex and 31% of worldwide telecom revenue. The service providers represent a good mix of geographies (44% Europe / Middle East / Africa, 33% North America, 16% Central and Latin America, 7% Asia Pacific) and carrier types (37% competitive operators, 35% incumbent carriers, 19% cable operator, 9% wireless).

Service providers responded to a broad range of topics, from most critical SBC features and top SBC applications, to security concerns, timelines, network location plans, and perceptions of SBC vendors.