| 丂 | |

|

|

|

|

|

|

|

|

|

![]()

仠

40G丄100G偺岝僩儔儞僔乕僶乕巗応偼丄崱屻丄僱僢僩儚乕僋憰抲儀儞僟乕偺撪惢昳偑庡椡傪愯傔傞梊憐

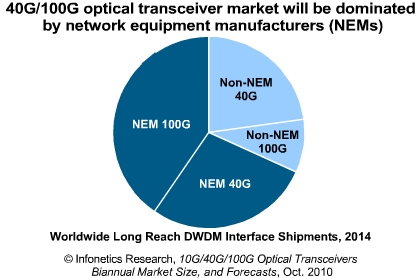

2010擭10寧28擔丄儅僒僠儏乕僙僢僣丄儃僗僩儞丗巗応挷嵏夛幮偺Infonetics Research偼丄杮擔丄嵟怴偺10G/40G/100G岝僩儔儞僔乕僶乕偺巗応婯柾偲崱屻偺尒崬傒偵娭偡傞敳悎傪儕儕乕僗偟傑偟偨丅偙傟偼丄10G丄40G丄100G偺岝僩儔儞僔乕僶乕偍傛傃僩儔儞僗億儞僟乕偑丄岝僩儔儞僗億乕僩丄僉儍儕傾儖乕僞乕丄僗僀僢僠儞僌丄僄儞僞乕僾儔僀僘巗応偵偍偗傞斕攧幚愌傪捛愓偟偨摉奩嶻嬈暘栰偺嵟傕徻嵶側儕億乕僩偱偡丅丂偙偺儗億乕僩偱偼丄弶傔偰僉儍儕傾偵傛傞崱屻偺嵦梡寁夋偺梊憐丄僱僢僩儚乕僋憰抲儊乕僇乕乮NEM倱乯偵傛傞婇嬈撪愝寁丒惢憿偝傟偨40G丒100G偺弌壸梊應傕娷傓僐儞億乕僱儞僩梊應傪棫偰傑偟偨丅

傾僫儕僗僩偺尒夝

乽僱僢僩儚乕僋憰抲儊乕僇乕乮Alcatel-Lucent, Ciena, Cisco, Huawei, Infinera偲偄偭偨婇嬈乯偼丄塿乆弌壸偑憹戝偡傞40G偺Long-Reach億乕僩傪嫙媼偟偰偍傝丄2014擭傑偱100G億乕僩偺戝晹暘傪弌壸偡傞尒崬傒偱偡丅偙偺偙偲偼彜梡巗応偱晹昳儀儞僟乕偲尩偟偔嫞憟偡傞偙偲傪堄枴偟傑偡丅偙偺巗応偺尰幚偼丄偙偺椞堟偱搳帒偡傞嵺偼丄徻嵶偵暘愅偟丄帪偵偼堷偒壓偑傞偙偲傪昁梫偲偟傑偡丅偦偆偱側偄偲僱僈僥傿僽側搳帒廂塿偵捈柺偡傞偙偲偑偁傝傑偡丅乿偲,Infonetics Research偺岝暘栰偺傾僫儕僗僩愑擟幰 Andrew Achmitt偼弎傋偰偄傑偡丅

岝僩儔儞僔乕僶乕巗応偺僴僀儔僀僩

- Infonetics Research偼丄10G丄40G丄100G僩儔儞僔乕僶乕丄偍傛傃僩儔儞僗億儞僟乕傪崌傢偣偨巗応梊應傪丄2014擭偵偼悽奅偱21壄4愮枩僪儖傑偱惉挿偡傞偲偟偰丄尒崬傪嫮壔偟傑偟偨丅

- 悽奅拞偺捠怣僉儍儕傾偵傛傞WDM憰抲偺憹壛偼丄2010擭慜敿婜偵僆僾僥傿僇儖僀儞僞僼僃乕僗偺媫懍側憹廂傪傕偨傜偟傑偟偨丅

- 夞慄嬈幰偼40G丄100G媄弍偺椉曽偺昡壙偵婎偯偄偰儀儞僟乕傪寛掕偡傞偨傔丄嵟弶偵100G媄弍傪採嫙偟偨憰抲儀儞僟乕偼丄40G偺宊栺偺応崌偲摨偠傛偆偵丄挿婜偵搉傞廂擖偺懡偔傪摼傞偙偲偵側傞偲梊應偟偰偄傑偡丅

- XFP宍幃偺僠儏乕僫僽儖僩儔儞僔乕僶乕偼丄ROADM儀乕僗偺僱僢僩儚乕僋偵偍偄偰婛偵恖婥偑偁傝捠怣僉儍儕傾偼丄傛傝峀斖埻偺憰抲偵摨挷惈傪晅壛偡傞偙偲偑偱偒傑偡丅偙傟偵偼丄IP/僀乕僒僱僢僩抂枛僗僀僢僠丄儖乕僞乕丄偝傜偵CMTS僿僢僪抂枛丄FTTH OLTs丄DSLAMs偵傕巊梡偱偒傑偡丅

- 僠儏乕僫僽儖XFP僩儔儞僔乕僶乕巗応偼丄2009擭偐傜2014擭傑偱丄117亾偺擭娫暯嬒惉挿棪(CAGR)偱憹戝偡傞偙偲偑尒崬傑傟偰偄傑偡丅

- Infonetics偼丄10G僀乕僒僱僢僩(10GE)偲8G媦傃16G偺僼傽僀僶乕僠儍儞僱儖傪墳梡偟偨儌僕儏乕儖偺摫擖偵傛傝丄2010擭偐傜2014擭偺娫偵丄10G SFP偲僩儔儞僔乕僶乕偺廂擖偑攞憹偟丄儐僯僢僩弌壸偑3攞埲忋偵憹壛偡傞偲梊應偟偰偄傑偡丅

- 揹巕惂屼傪尭傜偟偨掅僐僗僩峔憿(SFP+偲XFP)傊偺僔僼僩偼丄10G僐儞億乕僱儞僩壙奿傪媫懍偵堷偒壓偘傞偲尒崬傫偱偍傝丄偦偺寢壥丄弌壸検偼憹壛偟偰傕丄廂塿偼墶偽偄偵側傝傑偡丅

- 摿偵丄100G梡PM-QPSK僜儕儏乕僔儑儞乮DP-QPSK偲摨偠乯偑丄40G梡PM-QPSK偺傢偢偐2攞掱搙偺壙奿偱棙梡偱偒傞傛偆偵側傝丄掅壙奿LR-4僜儕儏乕僔儑儞偑巗応偵弌偨応崌(2011擭偐傜2013擭偺娫)偼丄100G媄弍偺惉挿偼丄40G偺傕偺傛傝偐側傝懍偄偙偲偑梊應偝傟傑偡丅

儗億乕僩奣梫

Infonetics偺10G/40G/100G Optical Transceivers儗億乕僩偱偼丄揙掙揑側暘愅丄巗応婯柾丄2014擭偺廂塿傗弌壸検傪捠偠偨梊應傪採嫙偟傑偡丅 傑偨丄儌僕儏乕儖丄斖埻丄攇挿丄偍傛傃抁拞挿婜偱岝僩儔儞僔乕僶乕偲僩儔儞僗億儞僟乕傪捛愓偟丄巗応暘愅傪峴偭偰偄傑偡丅

- 挷惍壜WDM(屌掕C-僶儞僪)丄1550nm丄1310nm丄偍傛傃850nm攇挿偵傛傞10G儌僕儏乕儖偼丄僼僅乕儉僼傽僋僞乕丄 300僺儞丄XFP丄Other(X2丄XENPAK丄夵椙NEM摍偱暘妱偝傟偰偄傑偡丅

- 挷惍壜100G儌僕儏乕儖偼丄1310nm丄偍傛傃850nm偺攇挿偱丄僼僅乕儉僼傽僋僞乕丄 100G DWDM丄夵椙NEM100GBase-LR4(暿柤4x25G non-return-to-zero丄傑偨偼NRZ)丄偍傛傃100GBase-SR10(捠徧10x10G)偱暘妱偝傟偰偄傑偡丅

岝僩儔儞僔乕僶乕巗応偱惢昳傪嫙媼偡傞儀儞僟乕偵偼丄Avago丄Emcore丄Finisar丄Fujitsu丄JDSU丄NeoPhotonics丄Oclaro丄Oplink丄Opnext丄Source Photonics, Sumitomo, WTD, Yokogawa 偦偺懠偑偁傝傑偡丅儗億乕僩偺億乕僩梊應偼丄Infonetics Research偺10G/40G/100G僱僢僩儚乕僋億乕僩梊應偵婎偯偄偰偍傝丄偦傟偼峀斖埻偺婇嬈丄夞慄嬈幰丄僗僀僢僠儞僌嬈幰丄岝僩儔儞僗億乕僩愝旛嬈幰偺孹岦傪廤栺偟偰偍傝傑偡丅

(尨暥)

40G, 100G optical transceiver market will be dominated by in-house vendors

BOSTON, Massachusetts, October 28, 2010-Market research firm Infonetics Research today released excerpts from its updated 10G/40G/100G Optical Transceivers Market Size and Forecast, the industry乫s most detailed report tracking 10 Gigabit, 40 Gigabit, and 100 Gigabit optical transceivers and transponders sold into the optical transport, carrier routing and switching, and enterprise markets.

The report is the first to use end-market projections of carrier preferences and equipment shipments to drive component forecasts, including shipments of 40G and 100G ports designed and manufactured in-house by network equipment manufacturers (NEMs).

ANALYST NOTE

乬Network equipment manufacturers -- such as Alcatel-Lucent, Ciena, Cisco, Huawei, and Infinera -- are supplying an increasing share of 40G long reach ports and will ship most of the 100G ports through 2014, posing a competitive challenge to component suppliers in the market. The reality of this market requires that optical component vendors measure twice and cut once when making investments in this area or face a negative ROI,乭 notes Andrew Schmitt, Infonetics Research乫s directing analyst for optical.

OPTICAL TRANSCEIVER MARKET HIGHLIGHTS

- Infonetics Research increased its forecast for the combined 10G, 40G, and 100G transceiver and transponder market, expecting it to grow to $2.14 billion worldwide in 2014

- An increase in WDM equipment spending by carriers around the world resulted in rapid revenue growth for colored optical interfaces in the first half of 2010

- Equipment vendors who offer 100G technology first will take the majority of long-term revenue as well as more 40G contracts, as carriers are making vendor decisions based on a dual evaluation of 40G and 100G technology

- Pluggable tunable transceivers in the XFP format, already popular in ROADM-based networks, allow carriers to add tunability to a wider range of devices -- including IP/Ethernet edge switches and routers, and eventually CMTS head-ends, FTTH OLTs, and DSLAMs

- The tunable XFP transceiver market is forecast to grow at a phenomenal 117% compound annual growth rate (CAGR) from 2009 to 2014

- Infonetics expects 10G SFP+ transceiver revenue to more than double and unit shipments to more than triple from 2010 to 2014, led by modules for 10 Gigabit Ethernet (10GE) and 8G and 16G Fiber Channel applications

- The shift to more compact form factors with fewer electronics (SFP+ and XFP) and lower cost designs will rapidly push down unit pricing for 10G components, resulting in flat revenue on increasing volume

- The ramp-up of 100G technology is expected to be faster than that of 40G, particularly when 100G coherent PM-QPSK solutions become available at a cost no more than double that of 40G coherent PM-QPSK, and when lower cost LR-4 solutions hit the market (2011 to 2013)

REPORT SYNOPSIS

Infonetics乫 10G/40G/100G Optical Transceivers report provides in-depth analysis, market size, and forecasts through 2014 for manufacturer revenue and units shipped. The report analyzes the market by module, reach, wavelength, and form factor, tracking the following long and short/intermediate reach optical transceivers and transponders:

- 10G modules by tunable, WDM (fixed C-band), 1550nm, 1310nm, and 850nm wavelengths, split by form-factor: 300 pin, XFP, SFP+, NEM-developed, and Other (including X2, XENPAK)

- 40G modules by tunable, 1310nm, and 850nm wavelengths, split by form-factor: DPSK, DQPSK, opto duo-binary (ODB) and other, NEM-developed, 300 pin SFI-5, 40GBase-LR4, and 40GBase-SR4

- 100G modules by tunable, 1310nm, and 850nm wavelengths, split by form-factor: 100G DWDM, NEM-developed, 100GBase-LR4 (aka 4x25G non-return-to-zero, or NRZ), and 100GBase-SR10 (aka 10x10G)

Vendors providing products in the optical transceiver market include Avago, Emcore, Finisar, Fujitsu, JDSU, NeoPhotonics, Oclaro, Oplink, Opnext, Source Photonics, Sumitomo, WTD, Yokogawa, and others.

Port forecasts in the report are based on Infonetics Research乫s 10G/40G/100G ports forecast, which aggregates trends from a wide range of enterprise, carrier routing and switching, and optical transport equipment.