| |

|

|

|

|

|

|

|

|

|

![]()

●

急成長する統合課金マーケットにおけるComverse とEricssonの接戦

カリフォルニア州キャンベル、2010年12月8日市場調査会社Infonetics Researchが、統合課金ソフトウェア及びサービス についての最新のマーケットシェアと予測リポートをリリースした。

本リポートは、プリペイド、ポストペイド、ハイブリッド・プリペイ/ポストペイ・モデルのような多数の決済方法による処理を可能にし、サービス方式(音声、動画、データ)、ネットワーク方式(有線、無線)、リージョンを横断する統合課金サービス(コンサルティング、インテグレーション、ホスト/マネージ・サービス)及び統合課金ソフトウェアについて詳細に観察している、統合課金マーケットを読み解く為の、当該業界の最も包括的なリポートである。

アナリストノート

「統合課金マーケットは特にダイナミックな市場であり、初期の実装は主として東南アジア、インド、東欧のように、オペレーターが激しい相場変動とARPUの低さに直面している新興市場で行われました。付加的マーケットの主導要因は機器間(M2M)牽引の、そして「モバイルウォレット」サービスの為の計算と請求を含むでしょう」Infonetics Researchの次世代OSS とポリシー担当主任アナリスト Shira Levineは指摘する。

統合課金マーケットハイライト

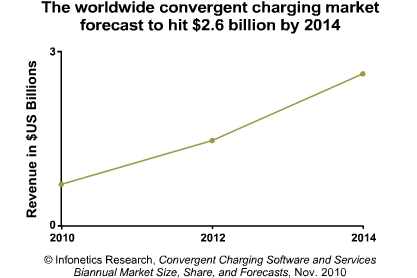

- Infonetics Researchは、ソフトウェアとサービスを含む世界的な統合課金マーケットが2009年から2014年の間に5億3300万ドルから26億ドルまで、約5倍近くに成長するであろうと予測する。

- 統合課金マーケット成長の主な牽引要因は、顧客のサービス短期乗り換えを防ぐ為の遠距離通信オペレーターによる攻勢、ロイヤリティプログラムによるユーザー当り収益(ARPU)の増加、そして柔軟な決済方法(例えば、時刻や加入者の居住地に基づいた、プリペイド・データとポストペイド音声、可変的価格設定を含むプラン)である。

- Comverse とEricssonは世界的な統合課金マーケットシェアのトップの座を競り合っており、Comverse が僅差でリードしている。

- マーケットの大部分がComptel 、 Openet 、Volubill、Orga Systemsを含む小さなソフトウェアベンダーで構成されており、その多くが新興・新規の市場に強固な足場を築いている。

- 多数のオペレーターが、全般的な操作環境、特に既存の請求能力に関する変更を必要とするだろう。

- スマートメーターとユーティリティー間、あるいはテレマティクスデバイスとフリート管理システム間のような機器間(M2M)取引が、いずれはモバイルネットワークにおける人間による支払処理容量を凌駕し、支払処理容量のその水準の根拠となり、一致させることを可能にする請求ソリューションの必要性を牽引するだろう。

- 例えばBest Buyは、Intec製の広告と請求ソリューションを、消費者の声やデータサービスの為だけでなく、家庭用器具のような接続されたデバイスも含むMVNO 戦略をサポートするために使用している。

レポート概要

Infonetics の年2回の 統合課金リポートは、統合課金ソフトウェアとサービスに関する世界的マーケットシェア及び、世界的・地域ごとの市場規模、分析、そして将来の予測を提供する。.

調査対象のベンダーにはAccenture、Acision、Alcatel-Lucent、Amdocs、Atos Origin、CapGemini、Cerillion、Comptel、Comverse、Convergys、Datatronics、Ericsson、Formula Telecom Solutions、Hewlett-Packard、Huawei、IBM、Intec、Logica CMG、Nokia Siemens、Openet、Oracle、Orga、Redknee、SAP、Tata、Tech Mahindra、Telcordia、TietoEnator、Volubill、ZTEその他が含まれる。

(原文)

Comverse, Ericsson neck and neck in fast-growing convergent charging market

Campbell, CALIFORNIA, December 8, 2010-Market research firm Infonetics Research released its updated Convergent Charging Software and Services market share and forecast report.

The report, considered the industry’s most comprehensive report on the emerging convergent charging market, takes an in-depth look at convergent charging services (consulting, integration, hosted/managed services) and convergent charging software that can handle multiple payment methods, such as prepaid, postpaid and hybrid prepay/postpaid models, across service types (voice, video, data), network types (wireline, wireless), and regions

ANALYST NOTE

“The convergent charging market is a particularly dynamic one, with early implementations occurring primarily in emerging markets, such as Southeast Asia, India and Eastern Europe, where operators are facing high churn rates and low ARPU. In the longer term, the additional market drivers will include accounting and charging for machine-to-machine (M2M) tractions and ‘mobile wallet’ services,” notes Shira Levine, directing analyst for next gen OSS and policy at Infonetics Research.

CONVERGENT CHARGING MARKET HIGHLIGHTS

- Infonetics Research forecasts the worldwide convergent charging market, including software and services, to grow nearly 5-fold between 2009 and 2014, from $533 million to $2.6 billion

- The primary driver for convergent charging market growth is the push by telecom operators to prevent customer churn and increase average revenue per user (ARPU) via loyalty programs and flexible payment methods (e.g., plans that include prepaid data and postpaid voice and variable pricing based on time of day or subscriber’s location)

- Comverse and Ericsson are neck and neck in the race for first place in worldwide convergent charging revenue market share, with Comverse holding a slight edge

- A sizable portion of the market is made up of smaller software vendors, including Comptel, Openet, Volubill, and Orga Systems, many of whom have a strong foothold in emerging and greenfield markets

- Operators’ cloud offerings will necessitate changes to their operational environments overall, and particularly to their existing charging capabilities

- Machine-to-machine (M2M) transactions, such as between smart meters and utilities, and between telematics devices and fleet management systems, will eventually far exceed human transactions on the mobile network, driving the need for charging solutions that can account for and reconcile that level of transaction volume

- For example, Best Buy is using billing and charging solutions from Intec to support its MVNO strategy, which will include not only consumer voice and data services, but also connected devices such as household appliances

REPORT SYNOPSES

Infonetics’ biannual Convergent Charging report provides worldwide market share and worldwide and regional market size, analysis, and forecasts for convergent charging software and services.

Vendors tracked include Accenture, Acision, Alcatel-Lucent, Amdocs, Atos Origin, CapGemini, Cerillion, Comptel, Comverse, Convergys, Datatronics, Ericsson, Formula Telecom Solutions, Hewlett-Packard, Huawei, IBM, Intec, Logica CMG, Nokia Siemens, Openet, Oracle, Orga, Redknee, SAP, Tata, Tech Mahindra, Telcordia, TietoEnator, Volubill, ZTE, and others.